These countries could lure manufacturing away from China

Call them “Altasia”

Mar 3rd 2023

SaveShare

Give

Alot of new portmanteaus have appeared in the pages of The Economist in recent years, many of them referring to phenomena in business and economics. Readers (and correspondents) have acquainted themselves with Bidenomics, permacrisis and DeFi. This week we came up with a new one: Altasia.

Short for the alternative Asian supply chain, Altasia is a result of the widening geopolitical rift between America and China. This is forcing global manufacturers to look elsewhere in Asia for new production sites. No single country in the region comes close to matching China’s importance as an export hub. But a crescent of 14 countries are together beginning to provide competition (see map).

How does Altasia compare with China? In exports they are evenly matched. Altasia shipped $634bn in merchandise to America in the 12 months to September 2022, a smidgen more than China’s $614bn. But China’s exports are more heavily weighted towards electronics, a vital category in which Altasia’s exporters do not all excel.

In terms of skilled workers, the two are also close. Altasia is home to 155m people aged 25 to 54—widely considered to be the prime working-age population—with a tertiary education. China has 145m.

The World Bank’s latest logistics-performance index from 2018, which measures countries on their efficiency in areas like customs, transport infrastructure and logistics regulation, shows the range of abilities across the region. China, with a score of 3.61 out of five, is ranked 27th among the 160 countries assessed. The Altasia nations range from Japan and Singapore, both in the global top ten with scores of 4.03 and 4.00 respectively, to 2.58 for Bangladesh and Cambodia, both in the lower half of the global rankings.

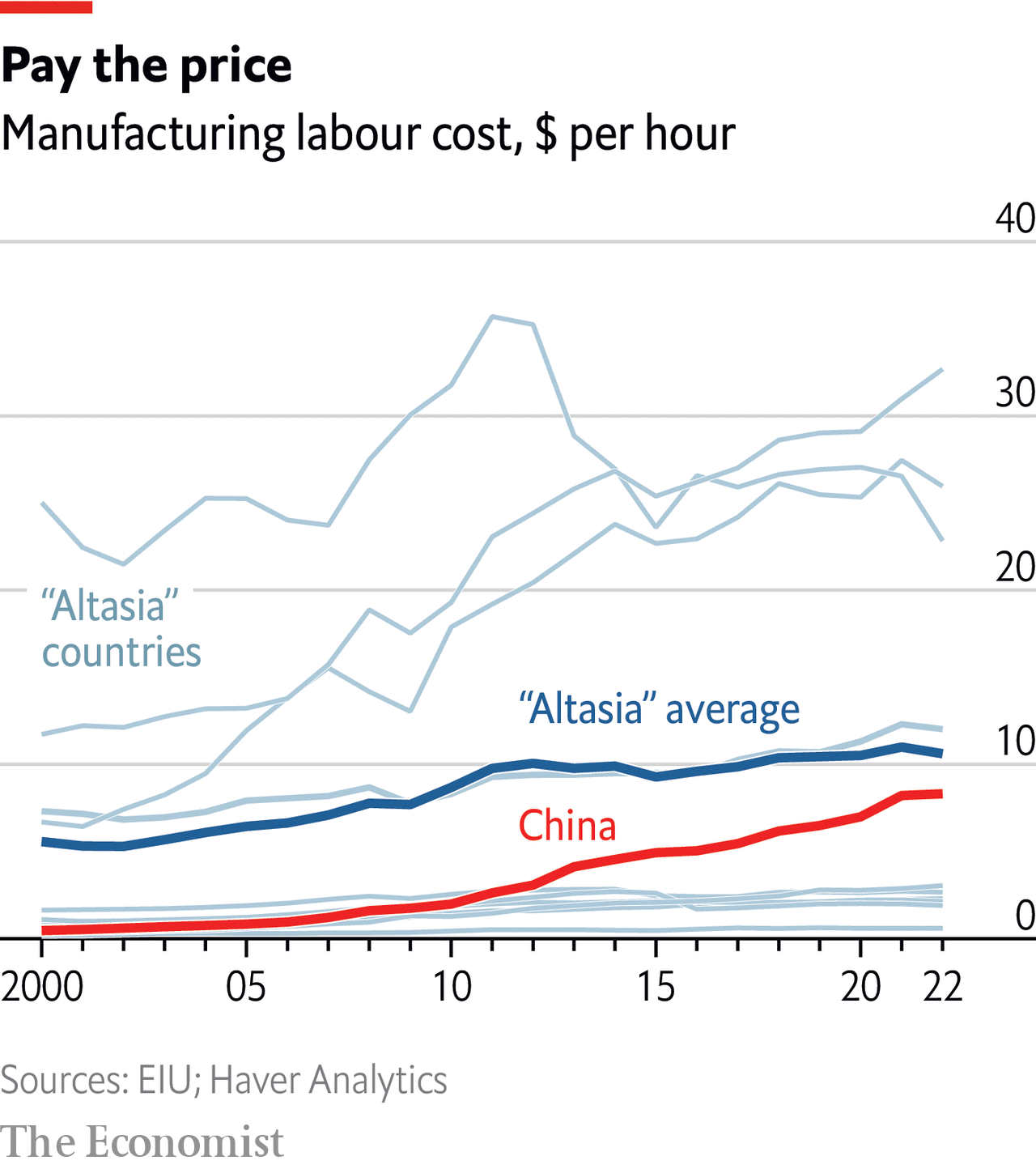

The great-power spat across the Pacific is not the only thing causing the shift. Labour costs in China have surged with the country’s increasing prosperity, and are now far higher than those in parts of South and South-East Asia (though workers in Altasia’s wealthiest countries, such as Singapore and Japan, earn far more). Manufacturing labour costs were $8.31 per hour in China last year, compared with less than $3 in places such as India, Thailand and Vietnam. Some manufacturers of lower-cost and lower-margin electronic goods were moving out of China even before the rift between China and America made it necessary.

Chinese production capabilities will be tough to replicate, however. The diverse economies of Altasia do not work together as a single entity the way China does. Infrastructure and logistics are huge challenges, though a number of trade pacts are easing regulatory barriers. But for many companies finding an alternative to China is now a priority. They are likely to be exploring opportunities in Altasia for years to come. ■